The year 2018 witnessed an increase in the office space leasing by 10 percent to over 20 million sq ft. This increase has been recorded in the first six months of this year. This clearly shows how the demand for co-working space is rapidly growing recently.

What is office space leasing/ co-working leasing? Nowadays, the trend of renting a space for business operations is growing day by day. With a number of startups coming up in the business world, the demand and need for working space is also increasing. And for this, the startups need to lease a portion of an office to carry on their operations. This process is called office space leasing.

According to the reports, the supply and leasing of co-working space saw an increase in these major nine cities including Delhi-NCR, Mumbai, Chennai, Kolkata, Bengaluru, Hyderabad, Pune, Kochi, and Ahmedabad.

The use of co-working spaces is anticipated to rise even more as the trend is being adopted not only by start-ups and individuals but also by well-established companies. This is expected to push up the share of co-working spaces in overall space leasing.

Here, we have a comparison between the previous and the current year’s stats and information about the office leasing space trend and how much the activity has increased since the last year on the basis of the major cities.

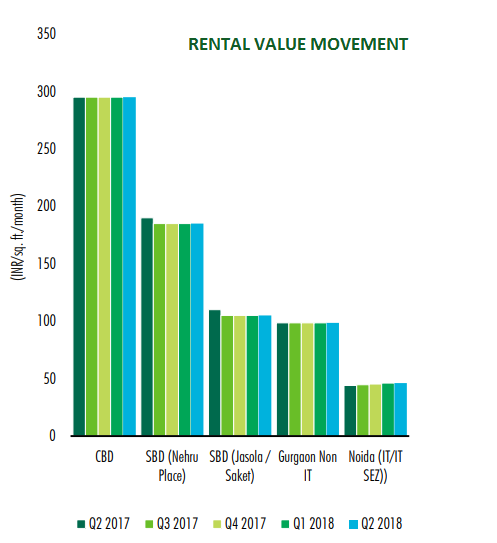

MARKET VIEW IN DELHI NCR

| 2017 | 2018 |

| – Gurgram dominated leasing activity; absorption grew on a q-o-q basis in Noida and Delhi.

– Rental growth in Golf Course Road and Noida Expressway (SEZ).

– Increased supply in the form of two small-sized IT developments on Noida Expressway, a medium sized non-IT development on Southern Peripheral Road, Gurgaon and a medium-sized IT development on NH-8.

– Engineering and manufacturing companies were dominant in the leasing activity with a share of about 25%, followed by IT/ITeS and e-commerce firms.

|

– Gurugram dominated leasing activity; q-o-q increase in leasing activity.

– Rental growth limited to select IT and SEZ developments in Gurugram.

– Increased supply in the form of one medium-sized SEZ development on Golf Course Extention Road in Gurugram, a medium-sized SEZ development on Noida Expressway.

– Co-working and business center operators were dominant in leasing activity followed by tech, research, consulting and analysis, and BFSI companies.

|

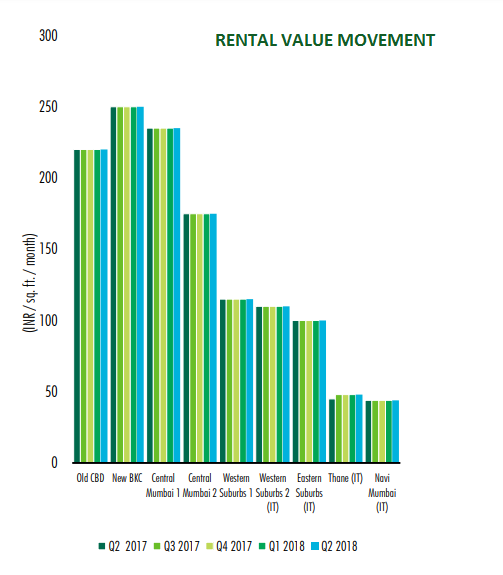

MARKET VIEW IN MUMBAI

| 2017 | 2018 |

| – Leasing activity declined marginally on a q-o-q basis.

– New supply added in PBD- Thane/Navi Mumbai and SBD – Andheri E.

– Stable rental values all over micro-markets.

– Occupiers from the BFSI sector were the biggest driver of space take-up, followed by infrastructure, real estate and logistics companies.

– Rental values were stable across all segments in all micro-markets of the city.

|

– Leasing activity declined marginally on a q-o-q basis.

– New supply added in Western Suburbs 1 and BKC periphery.

– Stable rental values all over micro-markets.

– Occupiers from co-working/ business center operators were the biggest driver of space take-up, followed by BFSI firms, small-to-medium sized firms.

– Rental values were stable across all segments in all micro-markets of the city. |

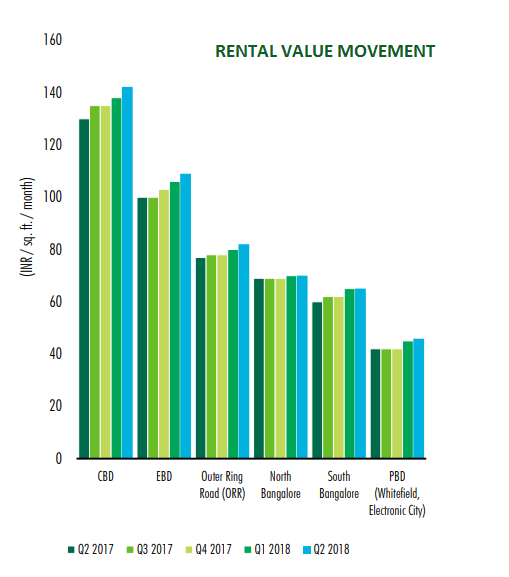

MARKET VIEW IN BENGALURU

| 2017 | 2018 |

| – Leasing activity increased on a quarterly basis.

– Supply completions across several micro-markets.

– Office space take-up remained largely concentrated in non-SEZ developments; with Sarjapur-Outer Ring Road (ORR) dominating leasing activity.

– IT/ITeS, BFSI and engineering and manufacturing firms dominated the office leasing space.

– Rental values rose by about 2 – 6% q-o-q across ORR, PBD, SBD and NBD. |

– Q-o-q decline in leasing activity.

– Supply additions in ORR, EBD, NBD and PBD.

– Office space take-up remained largely concentrated in non-SEZ developments; with ORR and NBD dominating leasing activity.

– Tech companies firms dominated the office leasing space.

– Rental values rose to 2-3% growth on a quarterly basis across non-SEZ buildings in CBD, EBD, PBD and ORR. |